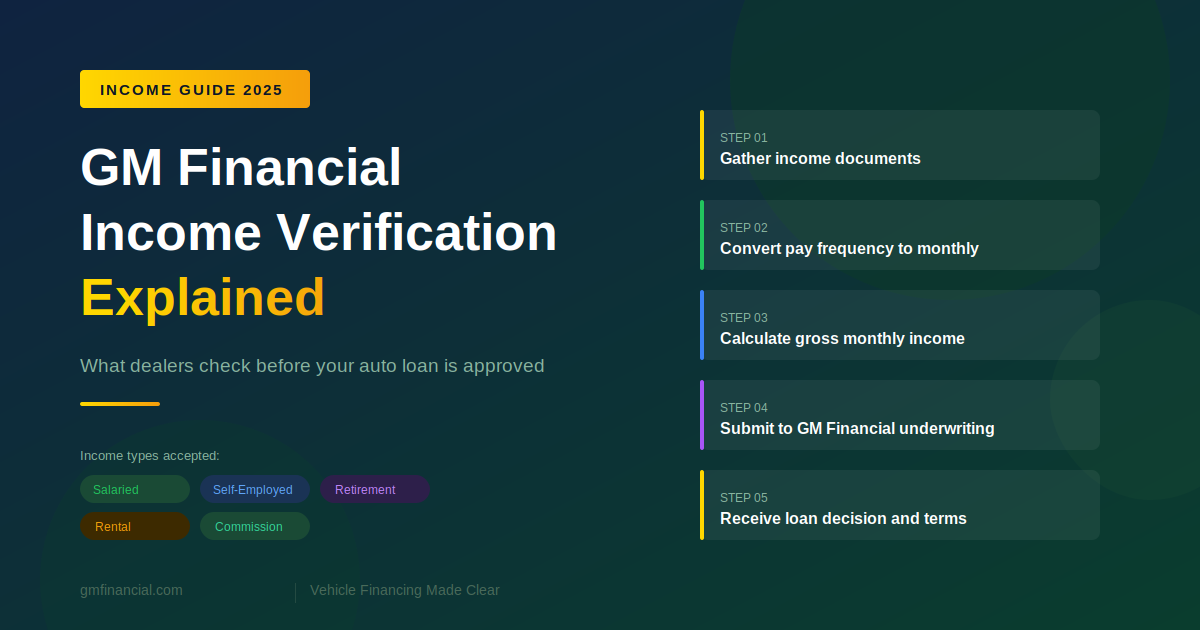

Buying a vehicle through GM Financial is one of the most common ways Americans finance a new or used General Motors product. Before any loan is approved, GM Financial requires proof that the applicant earns enough income to comfortably manage the monthly payments. This guide explains everything you need to know about how that income verification process works, what dealers look for, and how you can prepare to make the process as smooth as possible.

The Purpose of Income Verification in Auto Financing

Income verification exists to protect both parties in a financing agreement. For GM Financial, it confirms that the loan being issued is supported by the borrower’s actual earning capacity. For the buyer, it ensures that the loan amount offered aligns with what they can genuinely afford.

Without a reliable income verification process, lenders would have no objective basis for assessing loan risk. The result would be higher default rates, tighter lending standards across the board, and fewer buyers qualifying for financing at all. The structured approach GM Financial uses is what allows the lender to offer competitive terms to a broad range of buyers while managing risk responsibly.

The Core Income Types GM Financial Recognizes

GM Financial recognizes a wide spectrum of income types during the verification process. Understanding which category your income falls into helps you gather the right documentation before visiting the dealership.

Primary employment income is the most common type. This covers both salaried and hourly positions, full-time and part-time work. Secondary employment income, such as a second job or side work, can also be included if it is properly documented and shows a consistent history.

Self-employment income is evaluated differently from traditional employment income because it tends to be more variable. GM Financial typically averages self-employment income over 24 months using tax returns to arrive at a reliable qualifying figure.

Retirement income, pension payments, and Social Security benefits are accepted and are generally considered stable and predictable, which lenders view favorably. Investment income, rental income, and alimony or child support payments can also be included under the right circumstances with the appropriate documentation.

What Gross Income Means and Why Lenders Use It

When GM Financial calculates your qualifying income, the figure used is always gross income, not net income. Gross income is your total earnings before any taxes, health insurance premiums, retirement contributions, or other deductions are removed from your paycheck.

Many buyers are surprised to learn that lenders use gross income rather than take-home pay. The reason is that gross income represents your full earning capacity before discretionary and mandated deductions. It is a consistent baseline that allows lenders to compare applicants fairly regardless of their individual tax situations or benefit elections.

Your gross monthly income is the number that gets compared to your monthly debt obligations when the underwriter calculates your debt-to-income ratio. Keeping this ratio within acceptable limits is one of the most important factors in securing loan approval.

How Pay Frequency Affects Your Income Calculation

One of the most important and often overlooked aspects of auto loan income verification is pay frequency conversion. People are paid at different intervals, and the gross amount on any individual paycheck does not directly equal a monthly income figure without the right conversion.

GM Financial finance teams use standardized multipliers to convert pay stub amounts into consistent monthly figures. A weekly paycheck is multiplied by 4.33 to produce a monthly equivalent. A biweekly paycheck is multiplied by 2.167. A semimonthly paycheck is multiplied by 2. Only a monthly paycheck can be used directly without conversion.

Getting this conversion right is essential. An error in the pay frequency multiplier can result in an overstated or understated qualifying income, which could lead to approval for the wrong loan amount. This is why GM Financial’s standardized income tools are used consistently across all participating dealerships.

How Dealers Use Income Data Before Submitting Your Application

The dealership finance manager plays a critical role in the income verification process. Before your application is formally submitted to GM Financial, the finance manager conducts a preliminary income review using the tools available through the GM Financial dealer portal.

This pre-submission review serves several purposes. It allows the finance manager to identify any missing documentation before the application goes to underwriting. It also helps the manager advise you on which vehicles and loan structures are realistic given your verified income level. And it reduces the risk of a denial, which can have a short-term impact on your credit profile.

Experienced finance managers can often spot documentation issues quickly and work with you to resolve them before submitting. Bringing complete, organized documentation to your dealer appointment is the single most effective thing you can do to accelerate this process.

Variable Income: Overtime, Bonuses, and Commission

Many buyers earn income that varies from period to period. Overtime hours, performance bonuses, and commission-based earnings can represent a significant portion of total compensation but are treated differently from base salary or hourly wages during income verification.

GM Financial generally requires variable income components to be documented over a minimum of 24 months before they can be included in the qualifying income figure. This requirement exists because variable income is, by definition, not guaranteed. A strong quarter of commission earnings or a period of heavy overtime does not necessarily predict future income at the same level.

If variable income represents a meaningful part of your total compensation, having two years of pay stubs or W-2 forms that consistently show this income is your strongest tool for ensuring it is included in your qualifying figure.

Common Reasons Income Verification Gets Complicated

Several situations can introduce complexity into the income verification process. Changing jobs shortly before applying for a loan is one of the most common. While a new, higher-paying job is generally positive, lenders want to see stability, and a very recent employment start date may prompt additional documentation requests.

Gaps in employment history can also raise questions. If you took time off between jobs, be prepared to explain the gap and demonstrate that your current income is stable and sustainable.

Self-employment income is inherently more complex to document and verify than traditional employment income. Tax returns can show variable income from year to year, and business deductions can make taxable income appear lower than actual cash flow. Finance managers and underwriters who work with self-employed applicants regularly understand these nuances, and providing thorough, organized tax documentation helps immensely.

Preparing for Your Dealer Visit

The most effective preparation you can do before visiting a GM dealership for vehicle financing is to gather your income documentation in advance. For most employed buyers, this means your two most recent pay stubs. For self-employed buyers, it means two years of personal and business tax returns. For those with supplemental income sources, it means the relevant statements or award letters for each income type.

Arriving organized and prepared signals to the finance team that you are a serious buyer. It also compresses the time between sitting down at the finance desk and receiving a financing decision, which benefits everyone involved.

GM Financial’s income verification process is thorough because it needs to be. It is the mechanism that ensures loan decisions are grounded in real data rather than estimates. Understanding it from your side of the desk means you can engage with the process confidently, provide exactly what is needed, and move forward toward vehicle ownership with clarity and peace of mind.