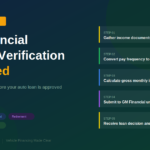

When you walk into a General Motors dealership and apply for vehicle financing, one of the first things the finance team does is verify your income. This step is not just a formality. It is the foundation on which your entire loan approval is built. GM Financial, the captive lending arm of General Motors, uses a structured and standardized income verification process to ensure that every buyer is approved for a loan amount they can realistically afford to repay.

Understanding how this process works puts you in a stronger position as a buyer. You will know what documents to bring, what figures matter most, and how the finance team converts your pay stubs into a qualifying income number. This article breaks down the full GM Financial income verification process from start to finish.

Why Income Verification Matters in Auto Lending

Lenders do not approve loans based on gut feeling. Every financing decision is supported by verified income data. GM Financial uses income verification to calculate your debt-to-income ratio, which compares your total monthly debt obligations to your gross monthly income. The lower this ratio, the stronger your application looks to the underwriter.

Income verification also protects you as a buyer. When a lender carefully confirms what you earn before approving a loan, it reduces the risk of you taking on more debt than you can handle. The GM Financial income verification process is designed with this balance in mind, serving both the lender and the borrower.

What Documents GM Financial Accepts for Income Verification

The type of documentation you need depends on how you earn your income. GM Financial accepts a wide range of income types, and each comes with its own documentation requirements.

For salaried and hourly employees, the two most recent pay stubs are typically sufficient. These stubs must show your year-to-date gross earnings, your pay frequency, and your employer information. If you have been at your current job for less than two years, the finance team may also request a prior employer letter or additional pay history to establish income stability.

Self-employed applicants need to provide two years of personal tax returns and, in most cases, two years of business tax returns as well. The lender uses these to calculate an average annual income, which smooths out any year-to-year fluctuations common in self-employment earnings.

Applicants who receive retirement income, Social Security, pension payments, or disability income need to provide award letters or benefit statements that confirm the amount and continuity of those payments. Rental income requires lease agreements and, in many cases, two years of tax returns showing the rental income reported.

How GM Financial Converts Your Income Into a Monthly Figure

Once your documentation is collected, the finance team uses standardized income tools to convert your raw pay data into a gross monthly income figure. This conversion is necessary because pay frequencies vary widely from one employer to another.

If you are paid weekly, your per-check gross amount is multiplied by 4.33 to arrive at a monthly equivalent. Biweekly pay, which arrives every two weeks, is multiplied by 2.167. Semimonthly pay, issued twice per month, is multiplied by 2. If you are paid monthly, your check amount is used directly.

This standardization ensures that a weekly-paid buyer and a monthly-paid buyer are evaluated on a perfectly level playing field, regardless of how their employer structures payroll.

How Year-to-Date Income Plays Into the Process

Your year-to-date gross income, shown on every pay stub, is a critical data point in the GM Financial verification process. The finance team uses this figure to cross-check whether your current income is consistent with what you earned last year.

If your YTD income annualizes to a figure that is significantly higher or lower than your prior year W-2, the underwriter will look more closely at the reason. A higher current income due to a recent raise or promotion may still be credited if it can be documented. A significant drop in income may prompt additional questions or documentation requests.

YTD analysis is also essential for buyers who earn overtime, bonuses, or commission income. GM Financial generally requires that these variable income components be documented over a 24-month period before they can be included in the qualifying income figure. A single large bonus or an unusually high overtime quarter will not automatically boost your qualifying income unless it reflects a consistent pattern.

The Role of the Dealer Finance Team in Income Verification

Your dealership’s finance manager is the first point of contact in the income verification process. Before submitting your application to GM Financial, the finance manager runs a preliminary income assessment using the tools available in the GM Financial dealer portal. This pre-screening step helps identify any documentation gaps before the formal application is submitted, saving time and reducing the chance of a denial due to missing paperwork.

The finance manager also advises you on which loan products align best with your verified income level. If your gross monthly income supports a specific payment range, the finance manager can model different loan terms, vehicle prices, and interest rates to help you find a financing structure that works within your budget.

What Happens After Income Is Verified

Once your income is verified and entered into the system, your application moves to the GM Financial underwriting team. The underwriter reviews your gross monthly income alongside your credit history, existing debt obligations, and the specifics of the vehicle being financed. All of these factors together determine whether your loan is approved, what interest rate you qualify for, and what loan terms are available to you.

Buyers who prepare their income documentation in advance consistently experience faster approvals and smoother deal closings. Knowing exactly what GM Financial needs before you arrive at the dealership removes friction from the process and puts you in the best possible position to drive away in your new vehicle.

Tips for a Smooth Income Verification Experience

Bring your two most recent pay stubs to the dealership. Confirm that each stub clearly shows your year-to-date gross income and your employer information. If you are self-employed, have your last two years of tax returns ready, both personal and business. If you have changed jobs recently, be prepared to explain the change and provide documentation from your new employer confirming your current salary or hourly rate.

Avoid gaps in your employment history where possible. Lenders view consistent employment as a positive indicator of income stability. If you have had a recent job change, being able to demonstrate that your new position pays as well or better than your previous one will strengthen your application considerably.

Income verification is not something to fear. It is a process designed to match you with the right financing for your situation. With the right preparation and a clear understanding of what GM Financial looks for, you can approach your auto loan application with full confidence.