Most employees look at one number on their paycheck — the deposit amount. But that number is the result of a chain of calculations that most people never fully understand. This guide walks through every layer of the calculation process so you know exactly where your money goes before it reaches your bank account.

Understanding the full tax picture is not just useful at tax season. It helps you make better decisions about retirement contributions, insurance choices, and even which job offer to accept.

How a salary paycheck is actually built

A salary paycheck does not start with your take-home pay. It starts with your gross pay — the agreed amount before anything is removed. From that number, your employer works through a series of deductions in a specific order.

The order matters because some deductions reduce your taxable income before federal and state taxes are calculated. Others come after taxes. Getting this order right is what separates an accurate paycheck estimate from a rough guess.

Step one: determine gross pay

For salaried employees, gross pay is simple. Take your annual salary and divide it by the number of pay periods in the year. If you are paid biweekly, that is 26 pay periods. Monthly is 12. Semimonthly is 24.

A $75,000 annual salary paid biweekly gives you a gross pay of $2,884.62 per check. That is your starting point — and every deduction that follows pulls from that number.

Step two: apply pre-tax deductions

Before any taxes are calculated, certain deductions are subtracted from your gross pay. These are called pre-tax deductions because they reduce the income figure that gets taxed. Common examples include:

- Traditional 401(k) or 403(b) retirement contributions

- Employer-sponsored health insurance premiums

- Dental and vision insurance premiums

- Flexible Spending Account (FSA) contributions

- Health Savings Account (HSA) contributions

- Commuter benefit deductions

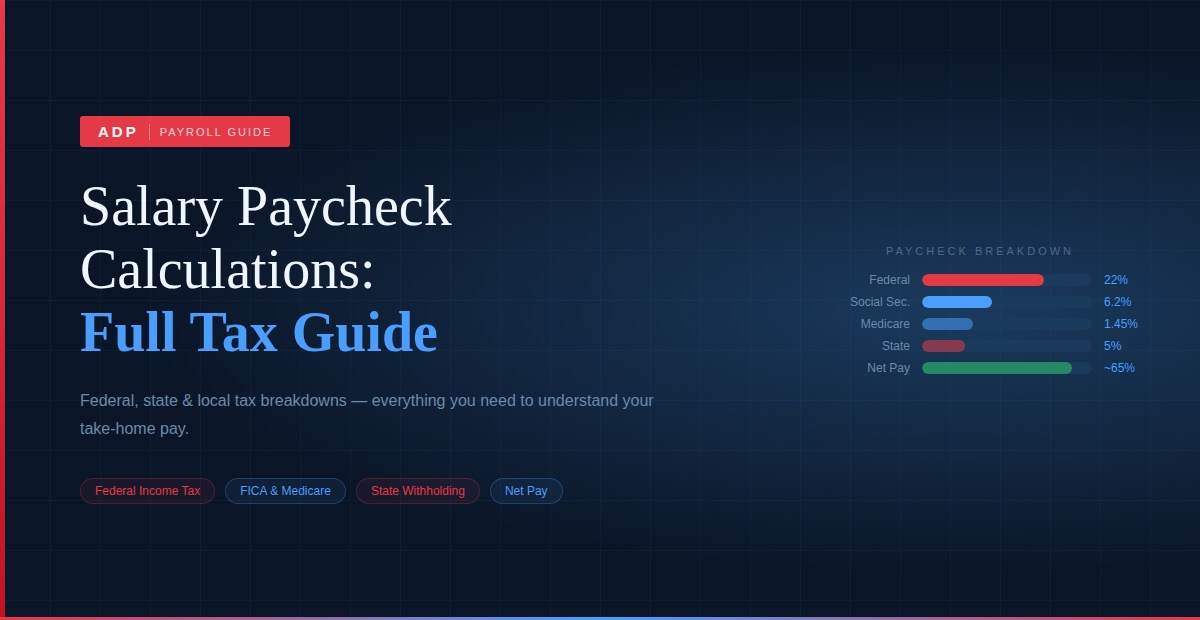

If your gross pay is $2,884 and you contribute $200 to a 401(k) and pay $120 for health insurance, your taxable income for that pay period drops to $2,564. That is the number federal and state taxes are calculated on — not the original gross.

Step three: federal income tax withholding

Federal income tax is calculated using IRS tax tables based on your filing status and the amount of your taxable pay. The US uses a progressive tax system, which means different portions of your income are taxed at different rates.

Your W-4 form tells your employer how to withhold. If you have allowances, additional withholding, or exemptions listed, all of those affect the federal tax amount deducted each pay period.

| Federal Tax Bracket (2024) | Single Filer Rate | Married Filing Jointly Rate |

| Up to $11,600 | 10% | 10% |

| $11,601 – $47,150 | 12% | 12% |

| $47,151 – $100,525 | 22% | 22% |

| $100,526 – $191,950 | 24% | 24% |

| $191,951 – $243,725 | 32% | 32% |

| $243,726 – $609,350 | 35% | 35% |

| Over $609,350 | 37% | 37% |

Remember — these are marginal rates. Only the income that falls within each bracket is taxed at that rate. A $75,000 salary does not mean you pay 22% on all $75,000. You pay 10% on the first bracket, 12% on the next, and 22% only on the portion that falls in that range.

Step four: FICA taxes

FICA stands for the Federal Insurance Contributions Act. It covers two mandatory payroll taxes that every employee pays regardless of state:

- Social Security: 6.2% on wages up to $168,600 per year (2024 wage base)

- Medicare: 1.45% on all wages with no income cap

If your annual wages exceed $200,000, an additional 0.9% Medicare surtax applies. These taxes do not change based on your W-4 elections. They are flat percentages applied automatically.

Step five: state income tax

After federal taxes, state income tax is calculated. Each state has its own rules. Some use flat rates — everyone pays the same percentage regardless of income. Others use progressive brackets similar to the federal system. And nine states charge no state income tax at all.

State taxes can range from zero to over 13%. For someone earning $75,000, the difference between living in Texas and living in California could mean thousands of dollars per year in additional state tax.

Step six: local taxes

Some cities and counties add a local income tax on top of state taxes. New York City, Philadelphia, Denver, and Detroit are among the most well-known examples. These local taxes are relatively small — usually between 1% and 4% — but they add up over a full year.

Most paycheck calculators do not automatically apply local taxes unless you specifically indicate your city. This is one reason actual paychecks sometimes differ slightly from calculator estimates.

Step seven: post-tax deductions

After all taxes are calculated and withheld, post-tax deductions are applied. Unlike pre-tax deductions, these do not reduce your taxable income. They simply come out of your after-tax pay. Examples include Roth 401(k) contributions, certain life insurance plans, and court-ordered wage garnishments.

What your pay stub is actually telling you

Every pay stub should show at least these items clearly:

- Gross earnings for the pay period

- Year-to-date gross earnings

- Each deduction itemized separately with amount

- Year-to-date deduction totals

- Net pay for the period

If any of these are missing or confusing, ask your HR department or payroll contact. You have a right to understand every line of your pay stub. Using a salary paycheck calculator helps you verify these numbers independently before there is ever a problem.

Why your paycheck changes throughout the year

Even if your salary stays the same, your paycheck amount can change during the year. Here are the most common reasons:

- Social Security stops being withheld once you hit the annual wage base ($168,600 in 2024) — your check gets slightly larger

- Health insurance open enrollment changes take effect mid-year

- A raise or promotion mid-year changes withholding going forward

- Bonus payments are taxed at a flat supplemental rate of 22% federally

- W-4 changes submitted to HR take effect on the next payroll cycle

See our main ADP Paycheck Calculator to run your own numbers and verify each of these scenarios with real figures.

Common questions about salary tax calculations

The new W-4 (redesigned in 2020) no longer uses allowances. Instead, it asks for specific dollar amounts for dependents, other income, and additional withholding. If you have not updated your W-4 recently, it may be worth revisiting to avoid a large tax bill or a smaller-than-expected refund.

Bonuses are considered supplemental wages. Employers typically withhold 22% in federal taxes on bonus payments — regardless of your actual tax bracket. This can cause some employees to receive less than expected from a bonus. The difference is reconciled when you file your annual tax return.

The total annual pay is the same either way. The practical difference is timing and budgeting. Biweekly gives you 26 checks per year — meaning two months each year you receive three checks instead of two. Semimonthly gives exactly 24 checks with a more predictable schedule. Neither is better for tax purposes.

This guide is for informational purposes only. Tax rates and rules change annually. Always confirm current figures with the IRS, your state tax authority, or a licensed tax professional.